Sacramento Leads, Central Valley Follows

More "we're not as bad as Sacramento" talk, this time from the Fresno Bee:

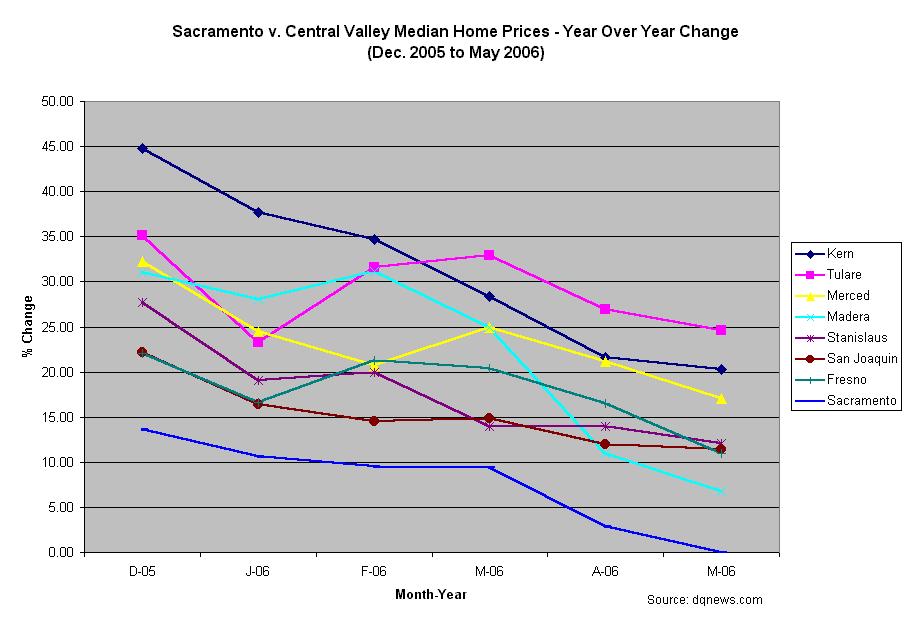

Values of new and used homes in the central San Joaquin Valley in May were still considerably higher than a year previously, which was a sharp contrast to some other regions of the state, data released Tuesday show...Hat tip: Ben Jones. While Sacramento may be ahead of the pack, that doesn't mean the rest of the Central Valley is immune from the current downturn. A look at the DataQuick numbers shows that appreciation has cooled even in the "hottest" areas over the last six months.

Property in the Valley appears to be holding its value better than some other parts of the state, especially around the capital. Prices in parts of Sacramento and Placer counties fell from a year previously. The median price in Placer County declined 2% from May 2005, with Auburn showing the sharpest drop -- 8% to $439,000. In nearby Fair Oaks, values fell almost 16%.

Based on all sales (SFHs, condos, and new homes)

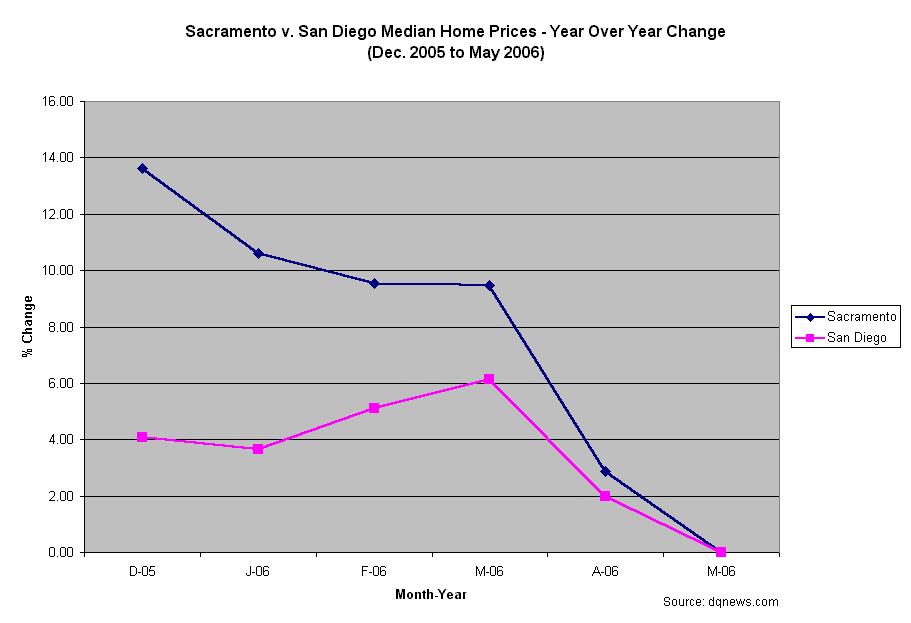

Based on all sales (SFHs, condos, and new homes)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}